Ferrari vs. Aston Martin

PART ONE: INTRODUCTION & COMPANY BACKGROUND

Founded in 1939 by Italian motor racer, engineer, and automobile designer Enzo Ferrari, Ferrari S.p.A is an Italian luxury car manufacturer based in Maranello, Italy. The firm produces high- performance grand tourers, supercars, and hypercars that embrace the firm’s rich history in both design and automobile racing. Originally, Ferrari became a public company in 1960, but in 1969, Fiat Chrysler Automobiles (FCA) purchased a controlling stake in the firm, leaving some minority ownership for Enzo Ferrari and his family. In 2016, FCA spun off Ferrari, giving each FCA shareholder one share in Ferrari S.p.A for every ten shares owned in FCA. Now, Ferrari’s top shareholders include the private equity firm Exor NV (17.3%) and Vice Chairman and son of Enzo Ferrari, Piero Ferrari (14.7%). Ferrari has established itself as a premier automotive manufacturer, combining power and elegance in its unrivaled engineering and timeless designs. The firm has won several accolades for its branding, including Brand Finance Global’s “World’s Strongest Brand” distinction in 2019 and 2020.

Aston Martin Lagonda Global Holdings Plc is a British luxury sports car and grand-tourer manufacturer headquartered in Gaydon, England. The firm was founded in 1913 by Lionel Martin and Robert Bamford, but the firm did not reach widespread status for its engineering and design capabilities until Sir David Brown took over in 1947 and shifted the brand’s identity to a more luxurious and expensive brand in the 1950s and 1960s. The firm’s current brands include the Vantage DB11, DBS, DBX, Valkyrie, and Valhalla. Aston Martin went public in 2018 by floating secondary shares on the London Stock Exchange, providing existing shareholders with liquidity, raising no new capital, and issuing no new shares. On its IPO date, Aston Martin shares opened at £19.00 and closed at £17.50, implying an 8.2% selloff on the first day of trading. In addition, the IPO famously cost Aston Martin £136.0 million, significantly impacting the firm’s 2018 financial results. Aston Martin’s top shareholders include the Saudi Arabian PIF (9.2%), chairman Lawrence Stroll (6.6%), and Mercedes-Benz Group AG (4.8%).

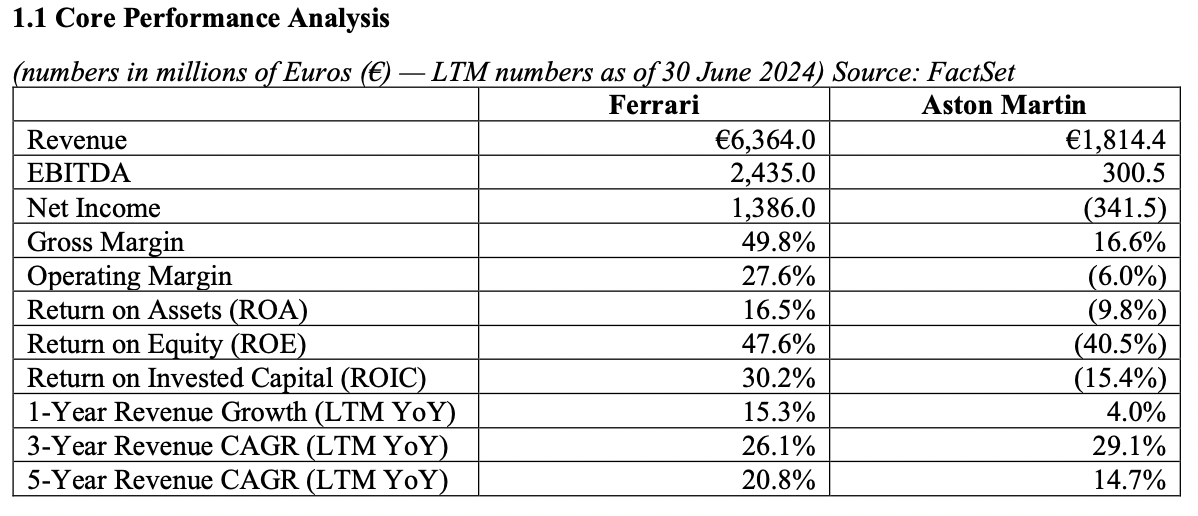

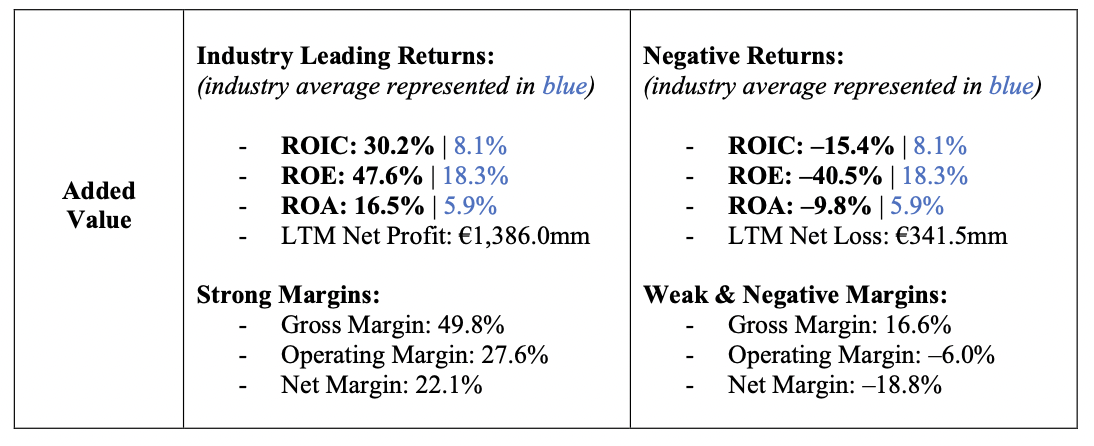

Ferrari’s recent financial performance demonstrates its strength in the luxury car market and superior brand image across the automotive manufacturing industry. Ferrari holds market shares — by volume of cars sold — of 24% in EMEA, 20% in the Americas, 43% in mainland China & Taiwan, and 38% in the rest of APAC. The firm has expanded this market share in the first three quarters of 2024, increasing YTD shipment volumes in all regions except for China & Taiwan. The Ferrari Purosangue, the Roma Spider, and the 296 GTS drove the increases in YTD vehicle deliveries.. Net revenues by region, expressed as a percent of total revenues, for FY2023 broke down as: [1] EMEA — 48.1%, [2] the Americas — 29.5%, [3] China & Taiwan — 9.8%, [4] APAC (excluding China & Taiwan) — 12.6%. Between 2021 and 2023, total revenues grew the fastest in Mainland China (92.5%) and in the United States (65.1%). Furthermore, Ferrari boasts significant profitability metrics as LTM (as of June 2024) ROA (16.5%), ROE (47.6%), and ROIC (30.2%) significantly outpace the industry averages of 5.9%, 18.3%, and 8.1%, respectively (2023 Annual Report).

Aston Martin’s recent financial performance demonstrates tumultuous demand, delivery delays, and the effects of its large debt burden. In November of 2024, executive chairman Lawrence Stroll adjusted the firm’s profit forecast downward, citing delays in the ultra-luxury Valiant models, supply chain disruptions in China, and demand erosion in China (Global Banking & Finance, 2024). In the end, Aston Martin downgraded its expected 2024 vehicle deliveries by 1,000 total cars. Net revenues by region, expressed as a percent of total revenues, for FY2023 broke down as: [1] EMEA (excluding the U.K.) — 33.5%, [2] the Americas — 27.7%, [3] APAC — 19.8%, [4] United Kingdom — 19.0%. Between 2022 and 2023, revenues increased in EMEA (excluding the U.K.) and in the Americas by 110.2% and 12.7%, respectively. Revenues in APAC and the U.K. declined by 8.6% and 15.3%, respectively. Overall, Aston Martin’s poor financial performance since its 2018 IPO has led to profitability metrics — ROA, ROE, and ROIC — falling well below the industry averages of 5.9%, 18.3%, and 8.1%, respectively.

PART TWO: INDUSTRY ANALYSIS

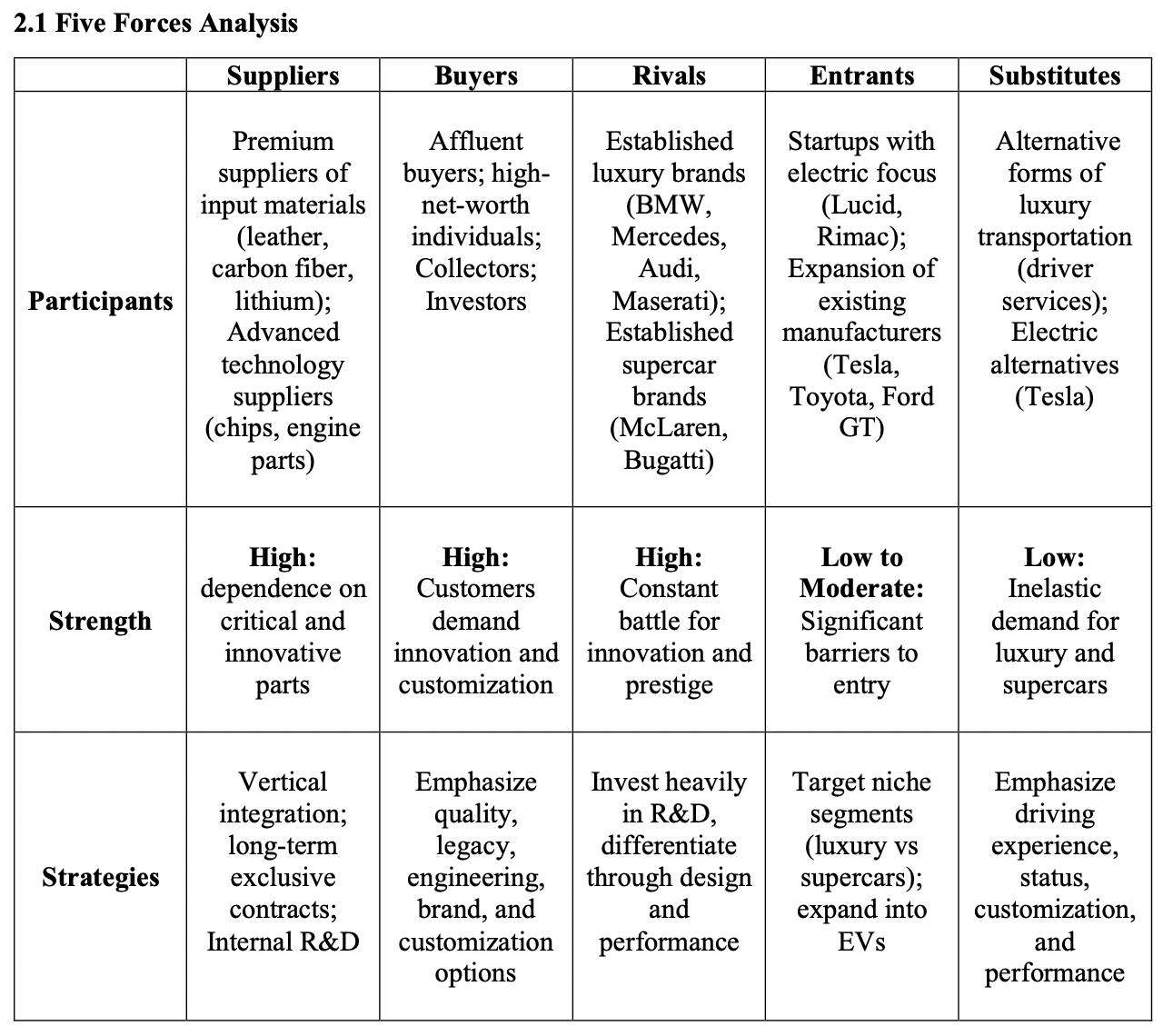

Ferrari and Aston Martin operate in the car manufacturing industry. Overall, the car manufacturing industry is characterized by intense competition and strong forces, requiring significant strategic navigation. Because of the intense structure of the industry, competitors have segmented the market and developed key areas of focus. Segments include mainstream vehicles, luxury vehicles, commercial vehicles, electric vehicles, off-road/utility vehicles, and high-performance sports/supercars. Ferrari and Aston Martin participate in the high-end luxury passenger vehicle and high-performance sports/supercar segments of the broader industry. In these segments, differentiation, product superiority, and branding determine which companies will be more successful. Other players in the luxury car segment of the market include Mercedes-Benz, BMW, Audi, Lexus, Maserati, and Jaguar Land Rover. Other players in the sport/supercar segment of the market include McLaren, Bugatti, Koenigsegg, Lamborghini, and Porsche.

2.2 How Market Factors Are Impacting The Five Forces

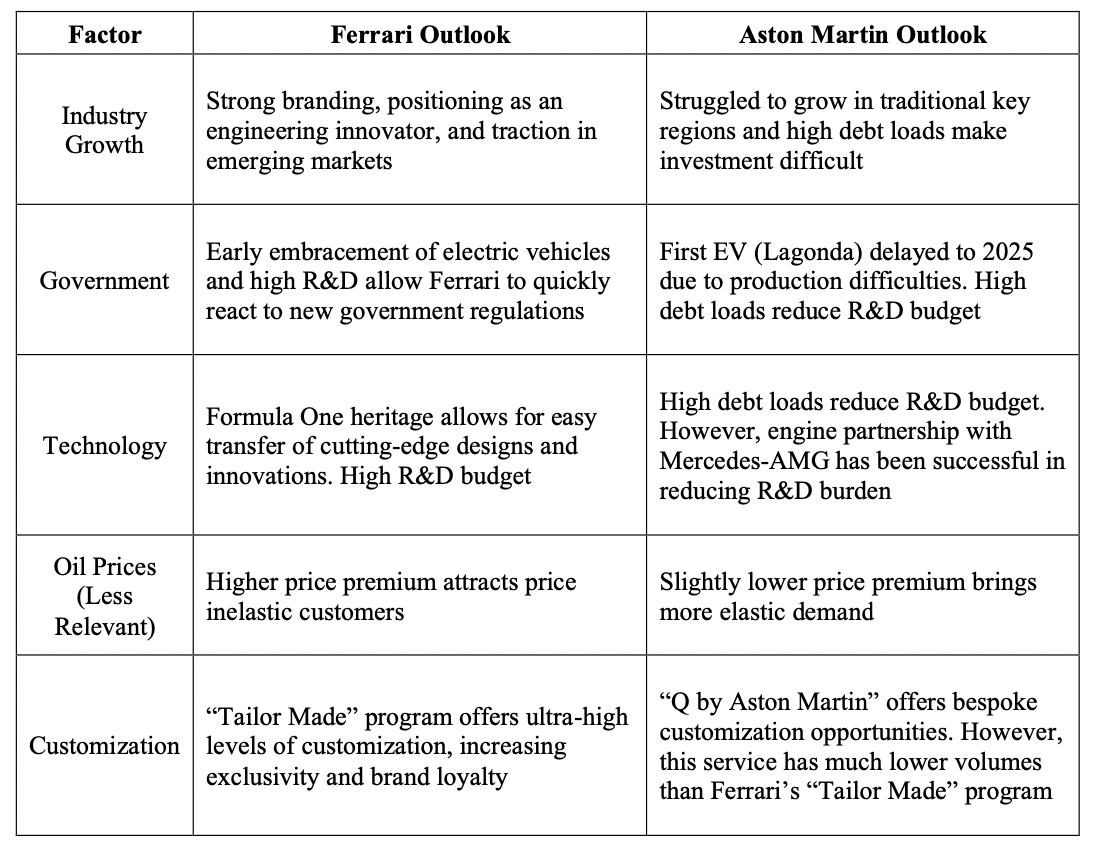

There are market factors of the car manufacturer market — specifically in the luxury and supercar segments — impacting Ferrari, Aston Martin, and all other market participants. Factors include industry growth, government/NGO regulation, technology and innovation, oil price volatility, and consumer trends. These factors impact industry forces. Thus, it is essential to understand how each factor an industry faces impacts the 5-force framework. Successful navigation of industry forces are how companies create a competitive advantage or identify a blue ocean strategy.

Industry Growth: The overall car manufacturing industry is valued at $2.8 trillion in 2024 with the expectation to grow to $6.5 trillion by 2032, implying a CAGR of 8.7%. More specifically, the luxury car segment of the broader car manufacturing industry was valued at $1.2 trillion in 2023, expected to grow to $2.8 trillion by 2032, implying a CAGR of 10.1%. The key factors to growth in the segment are electrification and customization. Affluent customers value the cutting-edge innovation of luxury vehicles and react positively to “exclusive” features and customization options. Furthermore, the supercar segment of the industry was valued at $17.0 billion in 2022 with the expectation to grow to $22.6 billion by 2031, implying a CAGR of 3.7% (Global Newswire, 2023). Industry growth impacts rivalry amongst competitors and the threat of new entrants. First, industry growth amplifies competitive rivalry because market participants fight to expand their market share to capture a disproportionate amount of growth. Increased rivalry would create races for innovation, luxury features, customization, and performance. Second, industry growth impacts the threat of new entrants by attracting new players looking to capture a portion of the overall market growth. However, the luxury and supercar segments have strong barriers to entry due to legacy brand names, but they are not fully insulated from new entrants, as evidenced by Rimac’s recent entrance into the electric supercar market. Despite this industry growth, each competitor’s unique strategy determines how much of the overall growth they can capture. The company with the best positioning and strategy will capture more growth while expanding its market share.

Government Regulations: Electric vehicle subsidies, the creation of “luxury car taxes,” and emission standards, are becoming more common in the car manufacturing industry. Recent regulations include the EU’s Euro 6 and Euro 7 emissions standards, the USA’s Corporate Average Fuel Economy Standards, and China’s New-Energy Vehicle Mandate. Each of these regulations imposes headwinds on the industry and impacts certain forces. Specifically, suppliers have more power as manufacturers begin to heavily depend on emission reducing inputs. Furthermore, regulations increase the bargaining power of buyers as they are more likely to purchase eco-friendly models that come with less of a tax burden. Finally, government regulations increase the threat of substitutes to traditional luxury cars by incentivizing electric alternatives.

Technological Innovation: Increased demand for technological innovation impacts all five of the competitive forces. First, Luxury and supercar manufacturers rely on suppliers for cutting-edge technology and consistent innovative features, forcing them to pay higher prices to suppliers. Second, buyers of luxury and supercars demand innovative products, increasing buyer expectations and influence. Third, the demand for innovation forces participants to compete for the top engineers. Finally, new advancements lower barriers to entry for new participants and make substitute products more plausible — as evidenced by Lucid Motors in the luxury electric vehicle market.

Oil Prices: Oil price volatility is a largely neutral factor in the luxury and supercar segments of the broader market because typical customers are affluent and price inelastic. However, it can impact the bargaining power of suppliers by forcing them to pass through higher costs onto the manufactures.

Customization: The increase in demand for customization in luxury vehicles and supercars impacts the traditional competitive forces landscape of the industry. Consumers are increasingly demanding features that cater to their unique tastes and preferences, increasing the bargaining power of buyers (Runbuggy, 2023). Furthermore, brands are competing to win customers by offering the most personalized cars, increasing the rivalry amongst existing competitors. For example, BMW offers fast and fully customizable vehicle delivery services in the United States through its South Carolina production facility (BMW, 2024).

Overall, Ferrari is better positioned to navigate the current market factors that are impacting the competitive forces in the luxury and supercar segments of the car manufacturing market.

PART THREE: COMPANY ANALYSIS – ASSESSING PERFORMANCE 3.1. Strategic Positioning

Ferrari and Aston Martin have the same target market — affluent buyers, high-net-worth individuals, collectors, and investors. This target market values technological innovation, engineering capabilities, branding, and luxury. Thus, Ferrari and Aston Martin focus on differentiation as their core value proposition. While each brand offers differentiated products from traditional manufacturers, each brand constantly differentiates their products by investing in engineering and innovation.

Ferrari and Aston Martin employ needs-based positioning, providing a range of products — grand touring vehicles, luxury SUVs, traditional sports cars, performance electric vehicles, and supercars — for a narrow target market. This positioning requires rapid innovation, attention to customer demands, and highly specialized product offerings. Thus, Ferrari and Aston Martin compete to win the business of a select number of buyers by offering the highest quality of goods and the most tailored products to these consumer’s direct needs.

3.1.1. Ferrari

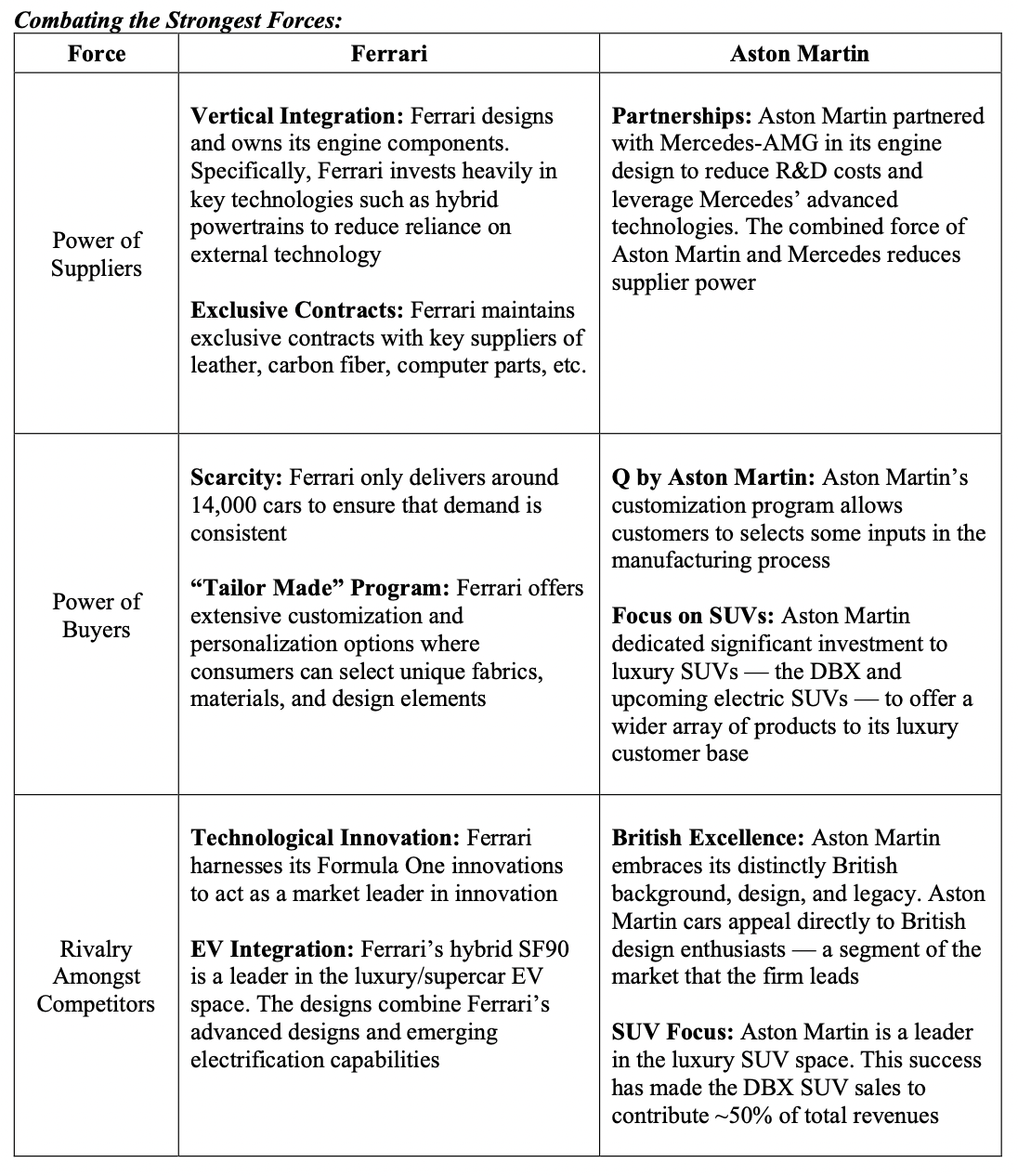

Ferrari’s strategic positioning is anchored around exclusivity and innovation. The firm limits production and dissemination of vehicles to ensure that demand constantly surpasses supply. In addition, the firm invests heavily in R&D to improve product quality and performance capabilities. Because of its exclusive and innovative positioning, Ferrari is able to command a significant price premium against competitors in the luxury and supercar segments of the industry.

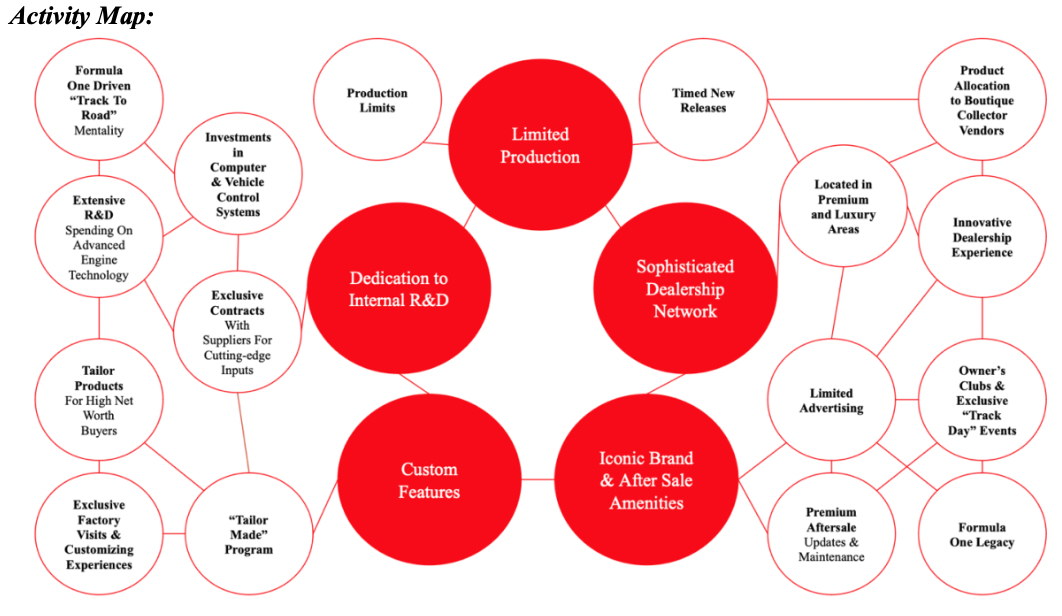

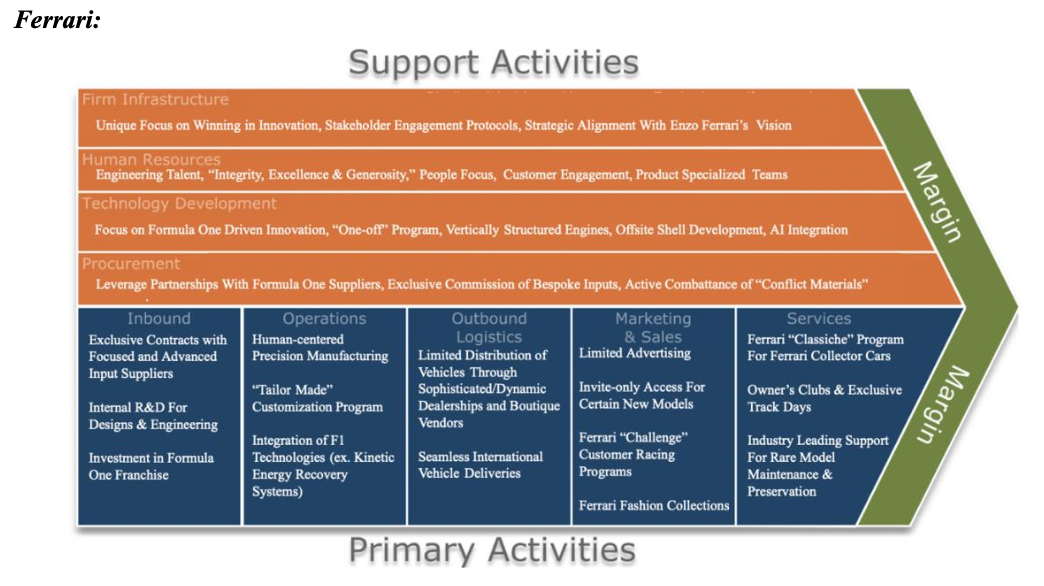

Ferrari’s main activities include [1] internal research and development, [2] limited production, [3] sophisticated dealership networks, [4] customization offerings, [5] after-sale brand management. First, Ferrari conducts most of its R&D research internally. Recent key areas of focus include hybrid systems, computerized vehicle control systems, advanced drivetrains, and enhanced track-focused aerodynamics. By owning the entire R&D process, Ferrari streamlines its technology and innovative ethos as well as protecting its technologies from being replicated by competitors. Second, Ferrari’s activities surrounding limiting production increase scarcity, allowing the firm to charge a higher premium. Third, Ferrari’s sophisticated dealership network emphasizes the luxury positioning of the brand and attracts high-net-worth individuals. Fourth, Ferrari’s customization activities increase brand loyalty and combat the market factor of increased demand for customization. Fifth, Ferrari engages in after-sale and brand management activities to provide maintenance and upgrades to its products, allowing the cars to maintain best-in-class performance. These activities also support brand loyalty as Ferrari owners gain access to exclusive events and owner networks.

Three Levels of Fit:

Ferrari employs all three types of fit — simple consistency, reinforcing activities, and optimization of effort. Ferrari’s consistent activities unanimously support its key areas of focus — innovation, exclusivity, and prestige — and the firm’s overall needs-based positioning. Furthermore, Ferrari’s activities reinforce each other, creating positive synergies and promoting innovation and exclusivity. For example, Ferrari’s Formula One (F1) program reinforces several activities. First, the program drives innovation in car performance and engineering, supporting the firm’s identity as an innovator. Second, Ferrari hosts track day experiences at F1 events, rewarding Ferrari owners and increasing preserved exclusivity. Third, Ferrari occasionally releases F1-inspired technologies and design elements in select new releases, adding scarcity and increasing customer’s willingness to pay. Moving to optimization of effort, Ferrari optimizes its activities by focusing on internal R&D. By creating innovative features internally, Ferrari creates direct and resilient exclusivity over designs and new technologies. Thus, Ferrari can focus on a leaner set of activities that create exclusivity and brand image. Other car manufacturers that rely on partnerships for innovation have fewer immutable designs and technologies, forcing them to brand-build or target even more niche segments of the market.

Tradeoffs & Sweet Spot:

Ferrari makes deliberate tradeoffs to maintain its competitive “sweet spot.” First, Ferrari limits its annual car sales despite strong demand to sell more vehicles. While selling more cars would improve revenues and spur significant growth, Ferrari chooses to limit the number of cars it sells to support its price premium, margins, and image as an exclusive brand. Second, Ferrari prioritizes customization over efficiency, slowing down the manufacturing process and increasing the cost of goods sold. Ferrari prioritizes customization over efficiency to continue charging significant price premiums and to deliver a unique purchasing and ownership experience. Third, Ferrari allocates a significant budget to its F1 program — a financial drain to the firm compared to exclusive focus on vehicle production. Ferrari allocates funding to its F1 program to create technology synergies that can be captured in traditional (non-F1) Ferrari vehicles. Success in the F1 program also improves the firm’s reputation for innovation and performance.

Based on these tradeoffs, Ferrari’s “sweet spot” lies in sacrificing scale, mass-market appeal, and ultra-efficient production techniques in favor of exclusivity, industry-leading innovation, and a bespoke customer experience. Ferrari’s carefully crafted ownership ecosystem fosters exclusivity and reinforces the brand’s mystique. Ferrari’s customer-centric model drives its success in the luxury and supercar segments of the car manufacturing industry.

3.1.2. Aston Martin

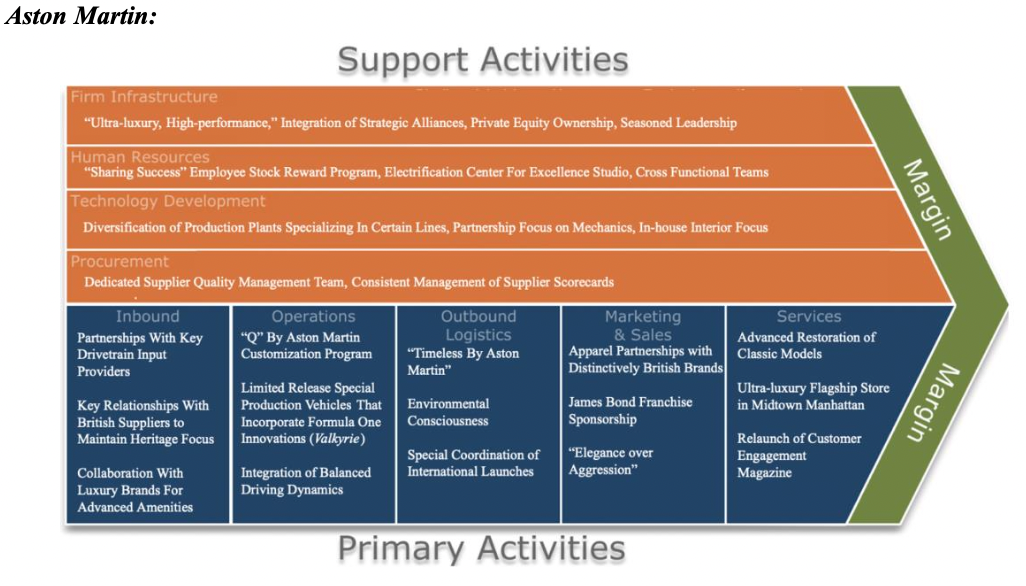

Aston Martin’s strategic positioning involves blending distinctively British luxury craftsmanship, partnership-driven performance capabilities, and lifestyle-oriented appeal. Aston Martin appeals to buyers who value luxury designs, heritage, and elegance over performance and technical sophistication. While Aston Martin develops technologically advanced supercars and track- worthy vehicles, the brand focuses on grand touring and lifestyle appeal. Aston Martin’s strategic positioning is very niche and less clear than other competitors. Ferrari positions itself as the pinnacle of performance, and Bentley positions itself as the pinnacle of luxury and comfort. Aston Martin falls between these participants as a “luxury-oriented” brand that still creates supercars and performance vehicles. Thus, Aston Martin has a comparatively weak strategic positioning.

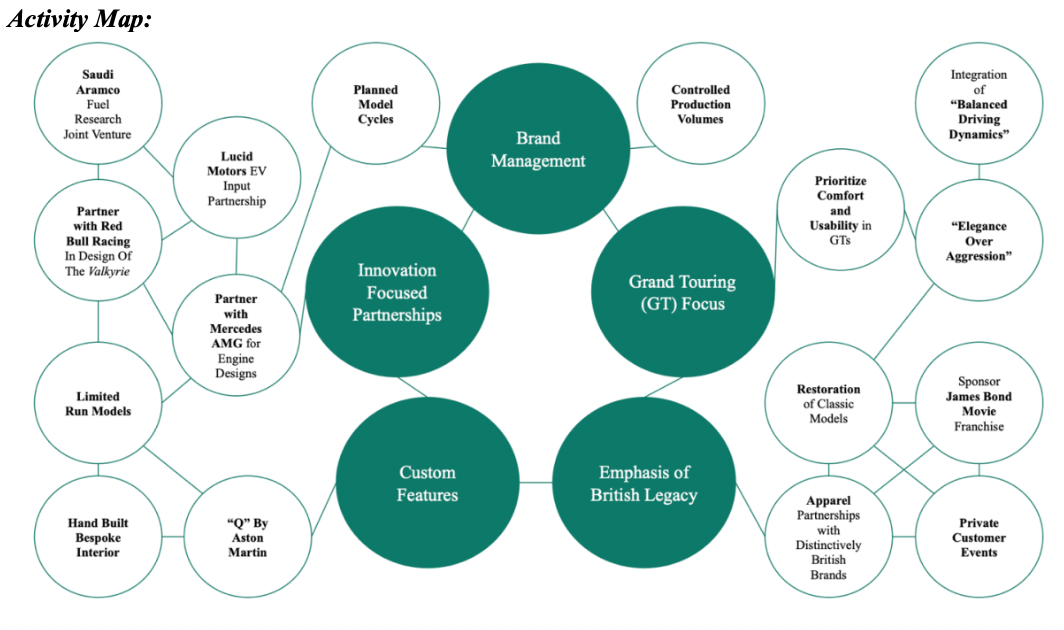

Aston Martin’s core activities include: [1] innovation-focused partnerships, [2] grand touring (GT) focus, [3] brand management, [4] emphasis on British legacy, and [5] customization. First, Aston Martin relies on partnerships with automotive innovators and engineering firms. These partnerships span across EV inputs, performance car designs, and environmentally friendly fuel research. While these partnerships address technical gaps, they suppress margins and reduce control over key technologies. Second, Aston Martin’s grand touring focus emphasizes luxury cars that support comfortable long-distance driving. GTs balance performance and comfort, reinforcing Aston Martin’s strategic positioning as a luxury-oriented brand. However, Aston Martin is lagging in electrification and managing competition in the GT space. Third, brand management activities increase the brand’s exclusivity and support the firm’s margins. Fourth, Aston Martin’s emphasis on British opulence supports brand image and margins. Fifth, Aston Martin’s “Q” program provides buyers the ability to customize their cars. This activity supports the firm in addressing the current customization trend amongst buyers. Together, these activities support Aston Martin’s strategic positioning as a luxury-oriented manufacturer with select performance models.

Three Levels of Fit:

Aston Martin somewhat employs two types of fit — simple consistency and reinforcing activities — and fails to employ optimization of effort activities. Activities such as partnerships, focusing on luxury GTs, offering limited run models, and dedication to “elegance over aggressiveness,” are consistent with the firm’s positioning as a comfortable luxury brand. However, Aston Martin’s partnerships erode the exclusivity impact of other activities — planned model cycles, controlled volumes, and private customer events. Furthermore, certain activities — hand-built bespoke interior inputs, the “Q” program, and “balanced driving” technologies — reinforce the firm’s simple elegance and luxury activities. However, activities such as the restoration of classic models and partnerships prioritize innovation, not elegance. Finally, the firm lacks overall optimization as activities diverge from the firm’s core focus. Partnerships, restoration of classic models, and limited deliveries accomplish different outcomes than “dynamic driving,” prioritization of comfort, and long- drive optimization activities. Overall, Aston Martin’s degree of fit reflects the firm’s volatile and largely inconsistent strategic positioning — straddling comfort/elegance and advanced performance. More successful car manufacturers have a more focused strategic positioning, allowing them to achieve better “fit.”

Tradeoffs & Sweet Spot:

Aston Martin’s main tradeoffs involve heritage/elegance over innovation and engineering prowess. The firm pursues timeless design and appeals to British opulence instead of investing in internal R&D. This tradeoff narrows Aston Martin’s buyer base to those who value classic appeal over innovation. In the same sense, Aston Martin has chosen to pursue GTs and SUVs more extensively than performance-driven supercars or traditional sports cars. This tradeoff will align the firm with its strategic positioning, but delays in its electric SUV and decreased demand for GTs have eroded recent sales projections in these segments. Aston Martin’s tradeoffs yield an implied “sweet spot” of appealing to legacy and elegance-driven customers. However, the firm is still trying to balance these core activities with innovation. Aston Martin is a British luxury icon, but it lacks any identity as a true innovator. This straddling of “sweet spots” has led to dismal financial projections and significant underperformance.

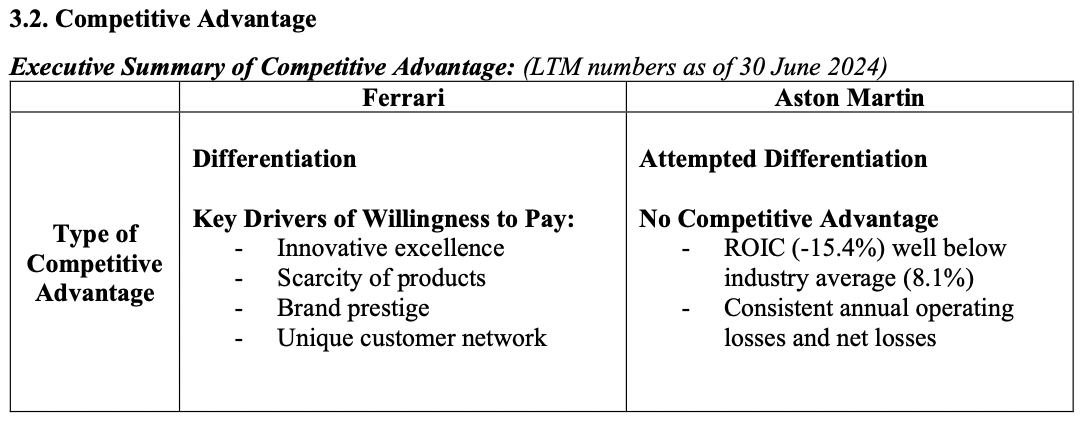

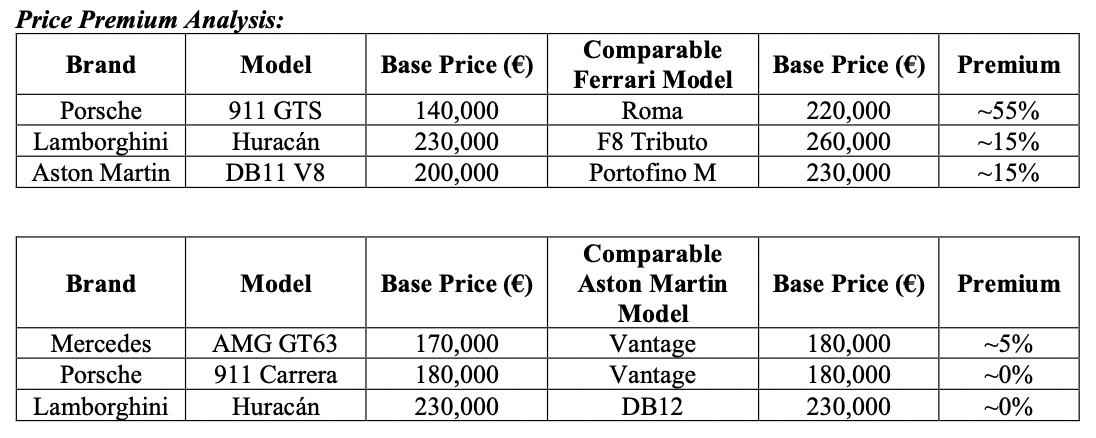

Ferrari is able to charge a price premium — evidenced by its higher pricing for comparable models. Aston Martin is unable to charge a price premium. Thus, Ferrari is better positioned as a differentiator.

3.2.1. Value Chain Analysis

3.2.2. Relative Costs Analysis

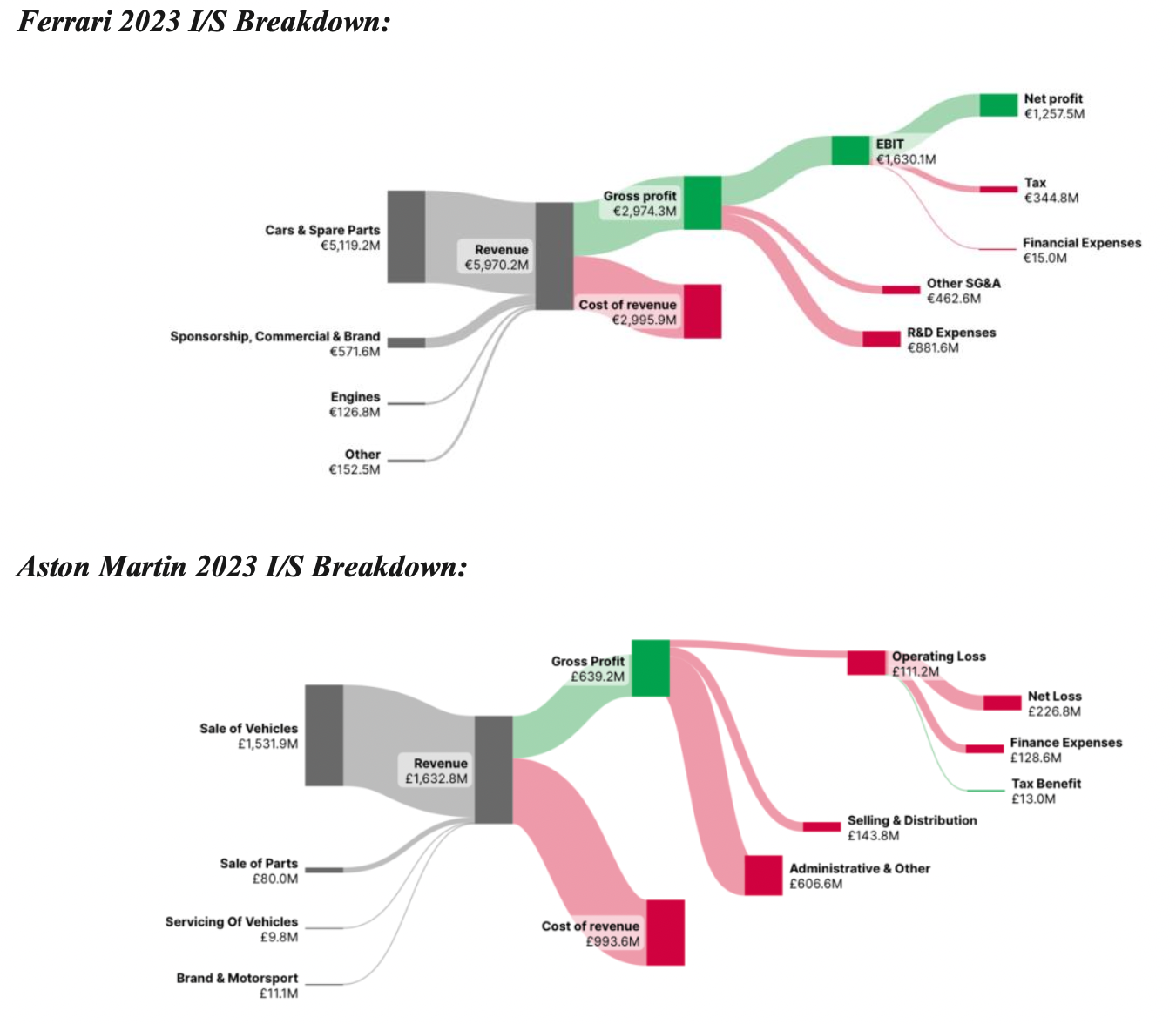

Ferrari is able to charge premium prices by increasing willingness to pay through its product superiority and innovative focus. This is evidenced by its higher gross margin (49.8%) and a lower COGS as a percentage of revenue (50.2%) compared to Aston Martin. In addition, Ferrari boasts a slightly lower SG&A expense as a percentage of revenue. While they are similar, R&D expenses accounted for the majority of Ferrari’s SG&A balance — implying significant reinvestment and strategic alignment with its positioning as a differentiator.

In addition, a research report from In Practise Research explains that Ferrari’s dedication to internal R&D capabilities has significantly capped variable costs associated with new car production. After incurring the initial cost of design development, Ferrari’s capital investment per car is roughly €57,000 to €58,000 versus €56,000 to €57,000 for Aston Martin. However, Ferrari is able to price each car at a significant premium to Aston Martin, creating a significant wedge per car. With Ferrari’s annual deliveries consistently outpacing Aston Martin, Ferrari is able to capture this wedge on a wider scale, leading to a distinct competitive advantage. While Ferrari is still forced to spend significantly more on the fixed cost of R&D, its unique designs and breakthroughs become stepping stones for future development and long-term assets for the firm.

3.2.3. Drivers of Willingness to Pay

Ferrari’s drivers of willingness to pay include: cutting-edge engineering, high-performance engines, and F1-developed technology; [2] scarcity of through its storied legacy, reputation for innovation and industry-leading performance, and [1] innovative excellence — driven by its products — created through limiting production and timed new releases; [3] brand prestige — formed customization options; [4] strong customer experience and network — driven by bespoke customization options and ownership clubs. These factors establish Ferrari as an industry-leading differentiator/innovator. In turn, Ferrari commands a significant price premium.

Aston Martin’s strategic positioning — straddling performance and luxury — has weakened the firm’s ability to create willingness to pay. Aston Martin is seen as a “luxury GT brand” as opposed to a consistent innovator and boundary challenger. Without the “halo effect” of ultra-innovative hypercars, brands including Ferrari and McLaren have outpaced Aston Martin in building a reputation as exclusive innovators. On the other hand, other brands, including Bentley and Rolls Royce, have outpaced Aston Martin’s luxury refinement and appeal. This erosion of clear brand identity has made it difficult for Aston Martin to command a consistently increased willingness to pay.

3.2.4. Evaluating Options & Making Choices

Ferrari’s key opportunities include: [1] high-performance electric vehicles, [2] high-performance luxury SUVs, [3] expanding geographic reach. Ferrari effectively entered the electric vehicle space with successful hybrid models — the SF90 Stradale and the 296 GTB. Ferrari can position new EV models as segment leaders, creating a “halo effect” for future expansion and directly competing with the Rimac Nevera and Tesla Roadster. Furthermore, the launch of the Purosangue SUV established Ferrari as a competitor in the high-performance luxury SUV space. Further expansion of capabilities and new SUV models could improve traction in specific markets and increase Ferrari’s TAM. Finally, Ferrari can leverage its strong strategic positioning to capture significant levels of industry growth in emerging markets. Specifically, China, the Middle East, and India represent a large opportunity for Ferrari to capture demand from affluent customers. Overall, Ferrari has immense opportunities in these underserved segments of the market, but competition remains fierce and rivals are responding to these opportunities. Aston Martin has similar opportunities as Ferrari; however, competitors’ responses will be more intense and difficult to overcome. For example, electrification is a key opportunity, but competitors such as Ferrari, Lamborghini, and Porsche have expanded their electric vehicle lineups and announced plans to further integrate electric capabilities into high-level models. Aston Martin has struggled with EVs recently, announcing a delay in its production to 2027 and citing underwhelming demand as the cause (Reuters, 2024). Instead, Aston Martin could shift its focus to even more underserved segments of the market. For example, Aston Martin could target female consumers — a buyer group generally ignored by luxury and performance car manufacturers. Furthermore, instead of pursuing EVs, Aston Martin could transition to other forms of eco-friendly practices that emphasize using clean materials and participating in carbon-neutral business practices.

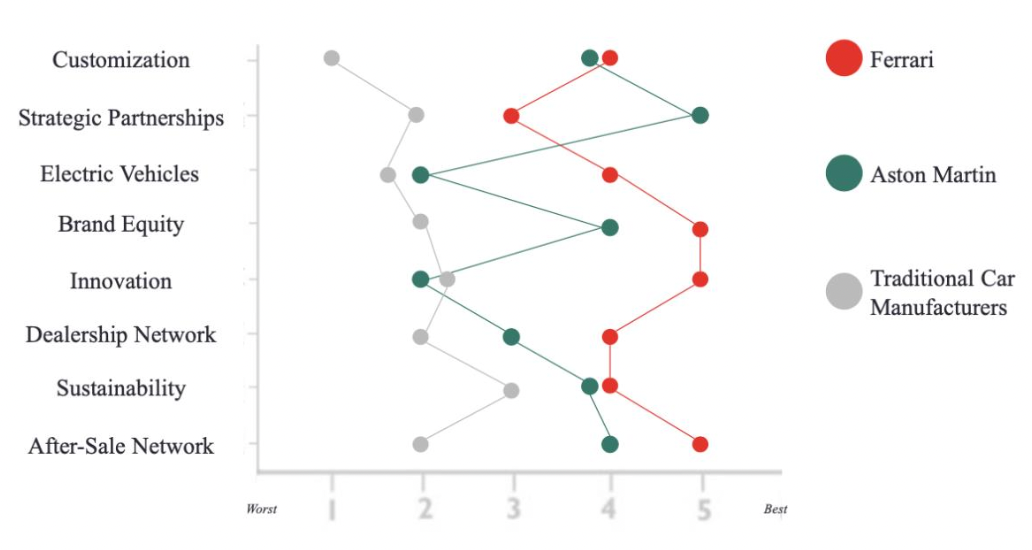

3.2.5. Value Proposition Diagram

The value proposition reflects Ferrari’s strong strategic positioning in the car manufacturing industry — specifically the luxury and supercar segments. Ferrari is a leader in several key areas: [1] customization, [2] brand equity, [3] innovation, [4] dealership network, [5] sustainability, [6] after-sale customer experience/network. Aston Martin performs well in strategic partnerships, leveraging key relationships with Mercedes, Red Bull Racing, and Lucid Motors to increase innovative designs and capabilities for customers. Overall, the Value Proposition Diagram demonstrates Ferrari’s distinct competitive advantage and unique ability to deliver value to customers.

3.3. Social Responsibility — Dual Purpose Playbook

Through its ESG initiatives, Ferrari demonstrates its commitment to both shareholders and stakeholders. Ferrari achieves impressive financial results while staying loyal to its ESG commitments. Aston Martin is comparatively weaker in its ability to pursue ESG initiatives due to EV production delays and financial constraints. Successful operation of this “dual purpose playbook” requires: [1] settling and monitoring financial and social goals, [2] structuring the organization to support the goals, [3] hiring, training, and socializing employees, [4] establishing dual-minded leadership.

3.3.1. Ferrari

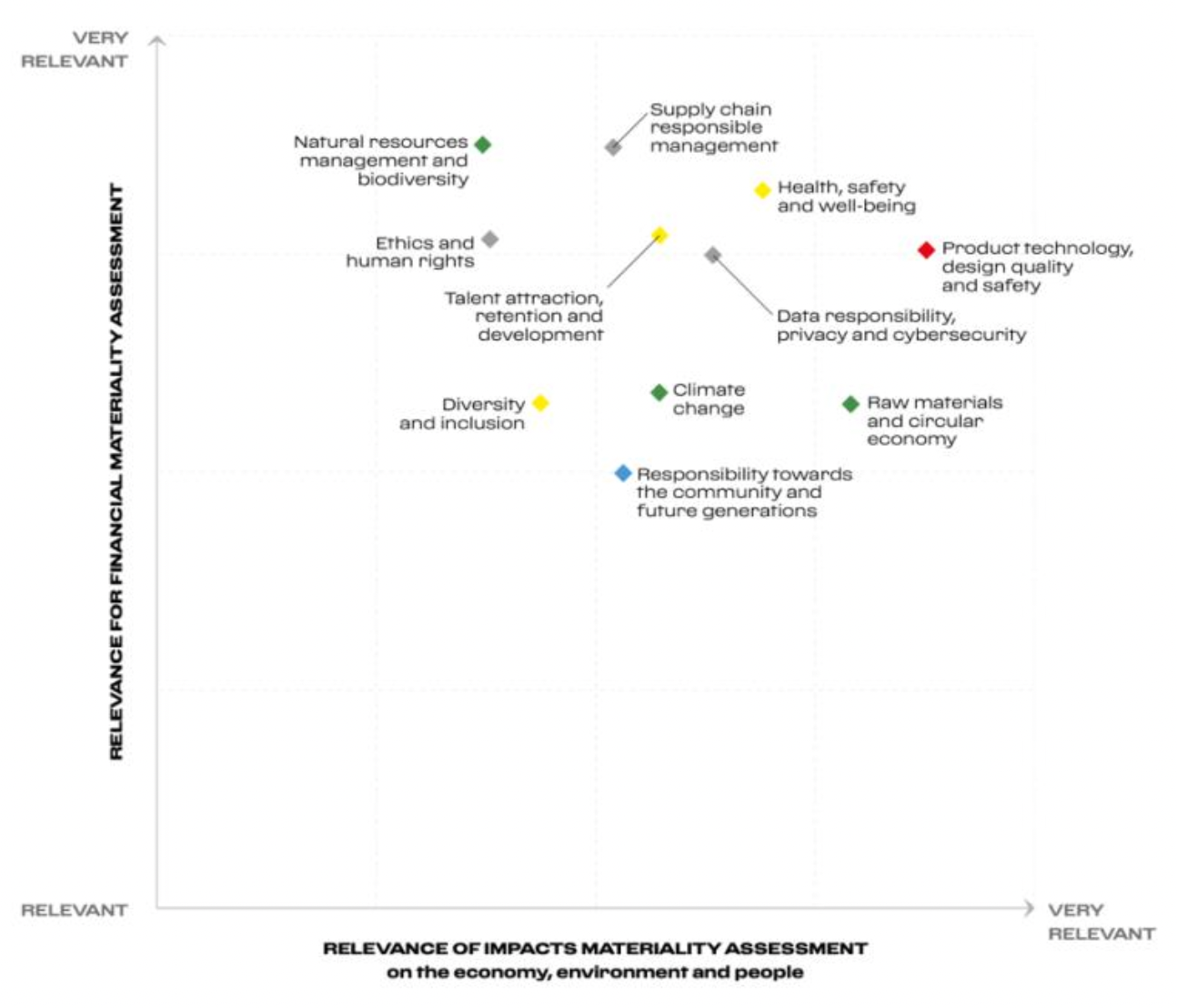

Setting and Monitoring Goals: In 2023, Ferrari conducted a “double materiality analysis,” taking into consideration the guidelines of the European Sustainability Reporting Standards (ESRS). This analysis identified key areas of importance across long-term financial goals and social impact goals. The analysis yielded the following matrix (2023 Annual Report):

Using these findings and weighing areas of importance, Ferrari committed to several long-term goals. First, Ferrari committed to carbon neutrality by 2030 by reducing carbon emissions along its value chain and investing in electricity-based technologies. Specifically, Ferrari committed to a 90% reduction in Scope 1 & 2 emissions by 2030. Second, Ferrari committed to making roughly 30% of its new vehicle lineup hybrid or fully electric by 2030. Third, Ferrari committed to achieving a “zero-accident workplace” by optimizing safety precautions. Finally, Ferrari announced plans to increase female representation in the workplace and leadership roles by roughly 30%. Ferrari monitors these goals through annual studies, working with NGOs to obtain certifications, and conducting employee surveys (2023 Annual Report). Key KPIs include emissions per car and departmental total units of energy consumption. Ferrari balances these goals with benchmark innovation standards and self-sustaining project guidelines.

Structuring The Organization: Ferrari’s organizational structure and strategic focus align with both financial and social goals. First, Ferrari created a “Green Sustainability Steering Committee” to oversee ESG efforts and integrate them into decision-making processes. The committee is composed of representatives from several key functions, streamlining decision-making capabilities. Furthermore, the structure within the R&D unit prioritizes sustainability by mandating significant capital allocation to electrification, sustainable materials, and lowering emissions.

Hiring & Socializing Employees: Ferrari employs all 3 forms of hiring: hybrid, specialized, and blank slate; however, most hiring is specialized due to the advanced nature of the work. Ferrari employs hybrid hiring by attracting experienced engineers with backgrounds in innovative roles (R&D) and social responsibility dedicated roles (emissions reporting). These hybrid employees are important to the firm because they can navigate both innovation and social responsibility tasks. Next, Ferrari hires specialized talent for either the business side or social/ESG side. Most positions with Ferrari are highly specialized as employees focus on certain engineering projects and innovations. On the other hand, some employees specialize in ESG roles, tracking progress toward goals and holding teams accountable. Finally, Ferrari uses blank slate hiring to attract younger talent and develop their skills in both the business and social side of the firm. In regard to employee socializing, the firm organizes events for new hires and existing employees. Ferrari organizes site tours of the Maranello headquarters and flagship production facilities for new hires, immersing them in the company’s innovative ethos and brand positioning. In addition, Ferrari organizes events for its employees at Formula One races, and in December of 2023, Ferrari hosted the “Ferrari Light Experience” as a holiday event for employees at its flagship factory.

Leadership: Ferrari’s leadership and board of directors support the firm’s “dual purpose playbook” and follow through with commitments. Ferrari’s management team is steadfast in its commitment to electric vehicles, expanding the program beyond the successful launches of the hybrid models into fully electric vehicles to be introduced in 2025. Furthermore, Ferrari’s board oversees its “Green Sustainability Steering Committee,” enforcing representation requirements and ESG standards. By aligning Ferrari’s core strategic positioning with social standards, Ferrari’s leadership team effectively demonstrated its commitment to both shareholders and stakeholders.

3.3.1. Aston Martin

Overall, Aston Martin’s high debt load and delays in electric vehicle production constrain the firm’s ability to manage a “dual purpose playbook” and balance financial results with purpose-driven initiatives. Instead of pursuing widespread direct ESG investments, Aston Martin has turned to partnerships in an attempt to accomplish more than immediate financial results.

Setting and Monitoring Goals: Aston Martin’s “Racing. Green.” strategy outlines several clear firm-wide goals including achieving net-zero carbon emissions across its supply chain, social/employee workplace improvement standards, and certain electrification standards. Aston Martin tracks performance in these categories through ESG committees, but the firm lacks clear and specific KPIs compared to Ferrari (Aston Martin 2023 Annual Report). Structuring The Organization: Aston Martin established a “Board Sustainability Committee” to oversee the firm’s ESG strategy, but it lacks the cross-functionality aspects of Ferrari’s “Green Sustainability Steering Committee.” Aston Martin’s organizational structure is more decentralized, undermining the strategic alignment of the firm in terms of entity-wide sustainability efforts. Because each work group has a narrower task, Aston Martin’s overall governance is comparatively weaker than Ferrari’s (Aston Martin 2023 Annual Report). Hiring & Socializing Employees: Aston Martin’s best attribute is its hiring and employee management activities. Aston Martin employs all 3 forms of hiring: hybrid, specialized, and blank slate. The firm hires hybrid employees who can bridge technical support with social/ESG progress. However, Aston Martin does this at a much smaller scale than Ferrari because of its limited direct investment in electric drivetrains and renewable energy systems. Additionally, Aston Martin utilizes specialized and blank slate hiring by finding workers with unique skills or up-and-comers from STEM backgrounds. Finally, Aston Martin has sophisticated employee socialization programs with retreats, corporate events, and employee share purchase programs (Aston Martin 2023 Annual Report).

Leadership: Aston Martin is more decentralized than Ferrari, undermining the ability for leadership to have a significant role on ESG activities. Because ESG revolves around partnerships, Aston Martin’s leadership has comparatively less impact in ground-level social-driven innovation. Additionally, high levels of leadership turnover created more decentralization and disrupted the continuity of ESG initiatives.

3.4. Leadership

3.4.1. Ferrari

Ferrari’s CEO Benedetto Vigna took over the firm in 2021 and has been a successful leader. Vigna immediately optimized Ferrari’s organizational structure and realigned the firm’s brand identity. Vigna has been successful at setting the vision/goals and motivating employees. To do this, Vigna effectively used several of Goleman’s leadership styles, most commonly using authoritative and affiliative styles of leadership. Vigna deployed authoritative leadership in implementing a more disciplined production strategy, emphasizing his vision of realigning Ferrari’s positioning and branding to prioritize luxury appeal. Vigna placed a hard cap on annual production volumes, emphasized in-house R&D, prioritized long-term innovation over short-term profits, and tightly managed customer experiences and F1 branding (Wall Street Journal, 2024). As a result, Ferrari cars became more of a luxury item and the brand began to carry a reputation for exclusivity. This leadership style created a catalyst for change and motivated employees by reinforcing the firm’s ambitious goals and commitment to excellence. Furthermore, Vigna utilized the affiliative style of leadership to create harmony, build relationships, and improve communication within the firm. After starting as CEO, Vigna interviewed as many people as he could, and by the end of his conversations, Vigna had spoken to over 300 employees (Wall Street Journal, 2024). This campaign increased employee trust and furthered Vigna’s understanding of the business. In turn, employees became more trusting of Vigna, leading to increased efficiency and alignment with the firm’s mission. To increase employee trust, Vigna enacted a program to make Ferrari a “zero accident workplace” through better safety measures. Additionally, Vigna authorized employee track days, allowing employees to see the benefits of their hard work first-hand. Overall, Vigna’s use of authoritative and affiliative leadership contributed to the firm’s new vision and increased employee motivation.

3.4.1. Aston Martin

Unlike Ferrari, Aston Martin has observed a revolving door of CEOs and unsteady leadership. In September, Aston Martin appointed its fourth CEO in four years, hiring former Bentley CEO Adrian Hallmark to replace former Ferrari CEO Amedeo Felisa as he steps down. Overall, recent leaders have failed to set a clear vision, motivate, and manage change. In addition, several leaders overused the coercive style of leadership and failed to use affiliative and authoritative leadership. Specifically, Tobias Moers — CEO from 2020 to 2022 and former Mercedes AMG executive — employed a “do as I say” coercive style of leadership that clashed with the existing work culture of the firm. Instead of creating positive change and newfound motivation, this led to increased conflict and the departure of several key executives (Motortrend, 2022). Furthermore, existing executive chairman Lawrence Stroll has created volatility in strategy by failing to use proper authoritative leadership. Stroll has focused on raising financing for the struggling business, creating a strategic disconnect and unclear goals. Stroll has not aligned his workforce under one vision, and these problems have been enhanced by the revolving door of c-suite executives (The Guardian, 2022). In addition, Stroll’s focus on raising financing eroded his ability to inspire his workforce through affiliative leadership. Stroll’s lack of emotional management during the financial restructuring of the firm led to further fragmentation and decentralization. Overall, Hallmark is inheriting a tradition of failed leadership and will attempt to reinvent the Aston Martin work culture.

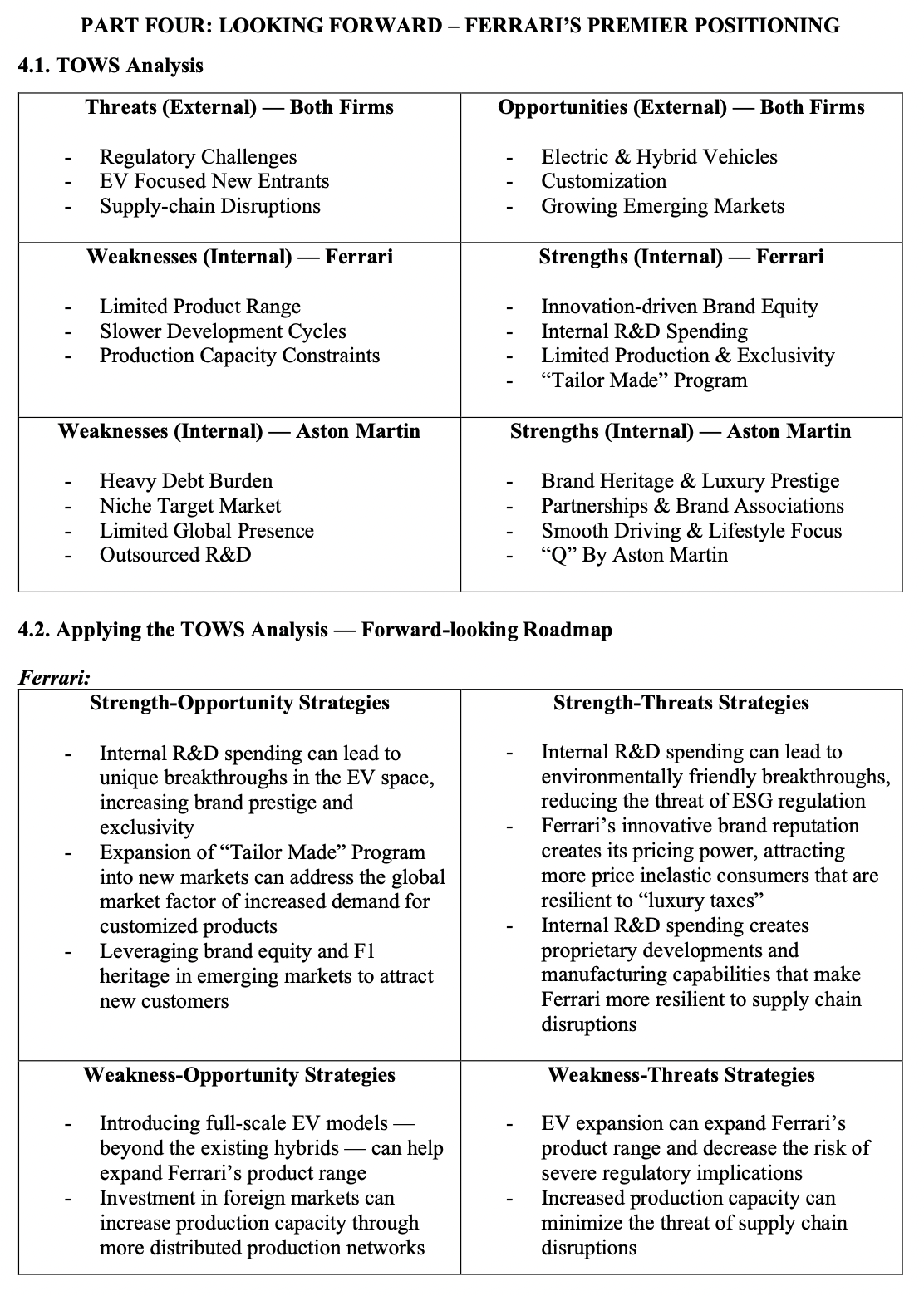

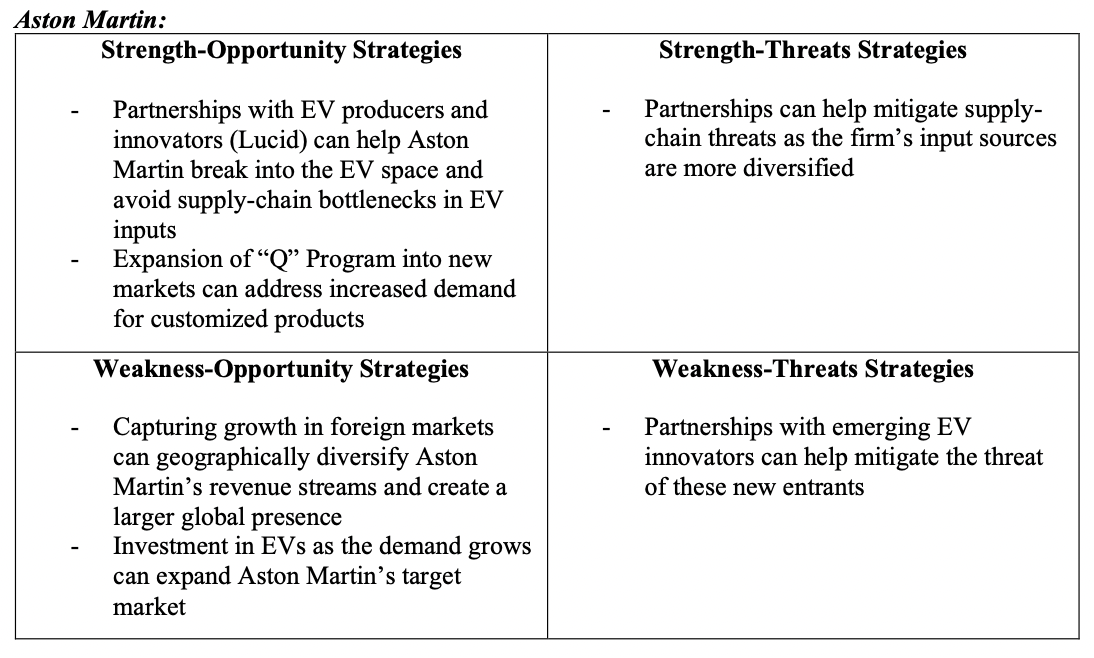

4.3. Conclusion & Final Outlook

In the competitive car manufacturing industry, Ferrari distinctively outperforms Aston Martin due to its comparatively stronger strategic positioning and ability to create and maintain a competitive advantage. Ferrari’s strategic positioning is anchored in exclusivity, innovation, and brand prestige. Thus, Ferrari attracts performance-focused customers who value cutting-edge designs, elaborate ownership networks, and a limited supply of cars. Aston Martin’s strategy is grounded in British heritage, luxury design, and comfort-focused innovation. Despite this, Aston Martin produces a select range of performance vehicles. Thus, Aston Martin’s overall strategy straddles luxury grand touring and high performance, undermining the clarity and focus of the brand. Focusing on competitive advantage, Ferrari’s differentiated activities centered around internal R&D-driven innovation, exclusivity, and customer loyalty have streamlined its relative cost base and increased customers’ willingness to pay, creating a distinct competitive advantage. Aston Martin’s reliance on partnerships, heavy debt burden, and lack of core strategic focus have led to high relative costs and the inability to create a willingness to pay; thus, Aston Martin has not been able to create a differentiation-driven competitive advantage. Overall, Ferrari’s advanced strategic positioning and demonstrated competitive advantage has led to superior financial results and clear leadership within the industry. Thus, Ferrari is better suited to be a long-term winner in the car manufacturing industry — specifically in the luxury and supercar segments of the broader market.

Due to its advanced strategic positioning and clear competitive advantage, Ferrari’sLTM (as of June 2024) ROA (16.5%), ROE (47.6%), and ROIC (30.2%) have significantly outperformed the industry averages of 5.9%, 18.3%, and 8.1%, respectively. This recent profitability underscores Ferrari’s ability to sustain its core competitive advantage. In its annual Capital Markets Day, Ferrari reaffirmed its commitment to keeping drivetrain and electrification capital spending in-house, continuing its key driver of success. In addition to profitability metrics, Ferrari outperformed Aston Martin in Gross Margin (49.8% vs. 16.6%), Operating Margin (27.6% vs. –6.0%), and Net Margin (22.1% vs. –18.8%). In contrast, Aston Martin’s financial performance is characterized by negative profitability and poor margins. Aston Martin’s ROA (–9.8%), ROE (–40.5%), and ROIC (–15.4%) fall well below Aston Martin has struggled to establish a clear strategic direction. Despite its heritage and distinctive British appeal, Analysts question the viability of Aston Martin continuing as a stand-alone entity due to high sensitivity to delays and adverse market conditions. Recent supply disruptions and demand shortfalls in China forced management to further downgrade 2024 financial projections — expecting about 1,000 fewer vehicles to be delivered than originally expected (Reuters, 2024). These sales projection downgrades supply disruptions and demand shortfalls not only eat into revenue expectations, but they add variable costs on core vehicle production, further eroding margin and the firm’s “wedge.”

In addition to its demonstrated success in strategic positioning and creating a competitive advantage, Ferrari’s value chain and operational strengths make it better prepared to navigate the changing industry landscape over the foreseeable future. Ferrari is better positioned to take advantage of opportunities, mitigate threats, and improve its weaknesses. Specifically, Ferrari’s key strengths make the firm uniquely able to capture market opportunities in electrification and untapped TAMs in emerging markets. These same strengths effectively mitigate the emerging threats of regulation, new EV-focused entrants, and supply-chain risks by allowing Ferrari to proprietarily develop regulation- friendly EV technologies that combat new entrants. Furthermore, Ferrari’s weaknesses are largely non-issues as they limit total production capabilities but reinforce scarcity and exclusivity. In comparison, Aston Martin is unprepared to navigate the fluid dynamics of the industry. Because of financial constraints and the negative impact of partnerships on margins, Aston Martin will not be able to effectively harness its strengths to address market opportunities or threats. Aston Martin’s strengths lack the true ability to address market opportunities or threats without additional liquidity injections. Without a unique ability to innovate and the capital required to expand into untapped TAMs, Aston Martin will continue to lose market share to more innovative participants. In addition, despite raising £1.9 billion of additional capital since its IPO, the firm continues to see production delays, market share loss, and increased reliance on partnerships. Overall, Ferrari’s robust strategic positioning, distinct competitive advantage, and strong financial performance indicate that the firm is well-equipped to successfully navigate the challenges of the car manufacturing industry. Aston Martin’s lack of clear strategic focus, heavy debt burden, and high propensity of production delays have led to poor financial performance and a weak strategic outlook.

Works Cited:

Aston Martin. ANNUAL REPORT 2023. https://www.astonmartin.com/- /media/corporate/documents/annual-reports/aston-martin-lagonda-annual-report-2023- interactive.pdf?rev=c186b2beb5614c3287a70399e312074e

Blackwood, Taylor. “The Growing Demand for a Personalized Vehicle.” RunBuggy, 29 Sept. 2023, runbuggy.com/the-growing-demand-for-a-personalized- vehicle/#:~:text=In%20today’s%20automotive%20world%2C%20the,trims%20to%20exclusive%20color%20palettes

“Car & Automobile Manufacturing Market Is Projected to Grow at 8.7% CAGR, Reaching US$ 6,457.67 Billion by 2034 | Fact.MR Report.” GlobeNewswire News Room, FACT.MR, 21 Nov. 2024, www.globenewswire.com/news-release/2024/11/21/2985077/0/en/Car- Automobile-Manufacturing-Market-is-Projected-to-Grow-at-8-7-CAGR-Reaching-US-6-457- 67-Billion-by-2034-Fact-MR-Report.html. Accessed 12 Dec. 2024.

Cohen, Ben. “He Loves Speed, Hates Bureaucracy and Told Ferrari: Go Faster.” WSJ, The Wall Street Journal, 20 Apr. 2024, www.wsj.com/business/autos/ferrari-cars-ceo-benedetto-vigna- 416e76d9?st=eui81vfuaaitmgk&reflink=desktopwebshare_permalink. Accessed 12 Dec. 2024.

FactSet. Historical financials for Aston Martin Lagonda Global Holdings PLC. FactSet, 2024, www.factset.com.

FactSet. Historical financials for Ferrari N.V. FactSet, 2024, www.factset.com.

Ferrari. FERRARI N.V. 2023 ANNUAL REPORT and FORM 20-F. 2023.

“Ferrari: Capital Efficiency.” Inpractise.com, 2019, inpractise.com/articles/ferrari-capital-efficiency. Accessed 12 Dec. 2024.

Goss, Louis. “Aston Martin Shares Fall 25% after Warning Blamed on Supply Disruptions, China.” MarketWatch, 30 Sept. 2024, www.marketwatch.com/story/aston-martin-shares-fall-25-after- warning-blamed-on-supply-disruptions-china-1d128bb1?utm_source=chatgpt.com. Accessed 12 Dec. 2024.

Jolly, Jasper. “Aston Martin Appoints Third CEO in Three Years as Tobias Moers Steps Down.” The Guardian, 4 May 2022, www.theguardian.com/business/2022/may/04/aston-martin-appoints- third-ceo-in-three-years-as-tobias-moers-steps-down.

“Luxury Car Market Size, Share, Trends | Growth Report [2032].” Fortunebusinessinsights.com, 2024, www.fortunebusinessinsights.com/luxury-car-market-104453#.

MacKenzie, Angus. “CEO Tobias Moers Leaves Aston Martin.” MotorTrend, 4 May 2022, www.motortrend.com/news/tobias-moers-leaves-aston-martin-ceo-amadeo- felisa/?utm_source=chatgpt.com. Accessed 12 Dec. 2024.

METAL - “TR 158 - Ferrari logo.” (n.d.). Tr-Finearts. Retrieved January 4, 2025, from https://www.thiagoromero.com/product-page/metal-tr-158-ferrari-logo

“Plant Spartanburg.” Www.bmwgroup-Werke.com, www.bmwgroup-werke.com/spartanburg/en.html.

Rajagopal, Uma. “Aston Martin Expects Lower Full-Year Core Profit as Delivery Delays Bite.” Global Banking | Finance, Global Banking and Finance, 27 Nov. 2024, www.globalbankingandfinance.com/aston-martin-expects-lower-full-year-core-profit-as- delivery-delays-bite/?utm_source=chatgpt.com. Accessed 12 Dec. 2024.

(Potts, Jeremiah, Strategic Management 3099, Boston College)